OPTIMAL INVESTMENT AND CONSUMPTION STRATEGIES WITH DEBT RATIO IN A STOCHASTIC VOLATILITY MARKET

DOI:

https://doi.org/10.60787/tnamp.v23.628Keywords:

Optimal investment, Optical consumption, Debt ratio, Stochastic volatility, Housing asset, Hamilton-Jacobi-Bellman equationAbstract

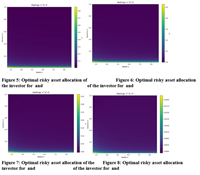

This paper investigates an optimal investment-consumption problem with endogenous leverage in a continuous-time market characterized by stochastic volatility and housing risk. We develop a unified framework in which an investor allocates wealth among a risk-free asset, a risky financial asset with Heston-type stochastic volatility, and a non-financial housing asset financed partly through debt. The investor simultaneously chooses the portfolio allocation, consumption rate, and debt ratio to maximize expected discounted utility under constant relative risk aversion preferences. Using stochastic dynamic programming, we derive the associated Hamilton-Jacobi-Bellman equation and obtain explicit closed-form solutions for the optimal portfolio policy, optimal debt ratio, and optimal consumption rule. The analytical results reveal that stochastic volatility affects investment decisions not only directly through the financial asset but also indirectly through leverage and housing exposure. Numerical illustrations demonstrate the sensitivity of the optimal policies to changes in volatility persistence, correlation structures, borrowing costs, and risk preferences.

Downloads

References

Merton, R. C. (1969). “Lifetime portfolio selection under uncertainty: the continuous-time case,” The Review of Economics and Statistics, vol. 51, no. 3, pp. 247–257.

Merton, R. C. (1971). “Optimum consumption and portfolio rules in a continuous-time model,” Journal of Economic Theory, vol. 3, no. 4, pp. 373–413.

Fleming, W. H. and Zariphopoulou, T. (1991). “An optimal investment/ consumption model with borrowing,” Mathematics of Operations Research, vol. 16, no. 4, pp. 802–822.

Vila, J. L. and Zariphopoulou, T. (1997). “Optimal consumption and portfolio choice with borrowing constraints,” Journal of Economic Theory, vol. 77, no. 2, pp. 402–431.

Dumas, B. and Luciano, E. (1991). “An exact solution to a dynamic portfolio choice problem under transactions costs,” The Journal of Finance, vol. 46, no. 2, pp. 577–595.

Shreve, S. E. and Soner, H. M. (1994). “Optimal investment and consumption with transaction costs,” Annals of Applied Probability, vol. 4, no. 3, pp. 609–692.

Liu, H. and Loewenstein, M. (2002). “Optimal portfolio selection with transaction costs and finite horizons,” The Review of Financial Studies, vol. 15, no. 3, pp. 805–835.

Dai, M., Jiang, L., Li, P., and Yi, F. (2009). “Finite horizon optimal investment and consumption with transaction costs,” SIAM Journal on Control and Optimization, vol. 48, no. 2, pp. 1134–1154.

Heston, S. L. (1993). “A closed‑form solution for options with stochastic volatility, with applications to bond and currency options,” The Review of Financial Studies, vol. 6, no. 2, pp. 327–343.

Fleming, W. H. and Herna´ndez-Herna´ndez, D. (2003). “An optimal consumption model with stochastic volatility,” Finance and Stochastics, vol. 7, no. 2, pp. 245–262.

Kraft, H. (2005). “Optimal portfolios and Heston's stochastic volatility model: an explicit solution for power utility,” Quantitative Finance, vol. 5, no. 3, pp. 303–313.

Chacko, G. and Viceira, L. M. (2005). “Dynamic consumption and portfolio choice with stochastic volatility in incomplete markets,” The Review of Financial Studies, vol. 18, no. 4, pp. 1369–1402.

Liu, J. (2007). “Portfolio selection in stochastic environments,” The Review of Financial Studies, vol. 20, no. 1, pp. 1–39.

Bank, P., Riedel, F. (2001). “Optimal consumption choice with intertemporal substitution”. Annals of Applied Probability, vol. 11, no. 3, pp. 750–788.

Jin, Z. (2014). “Optimal debt ratio and consumption strategies in financial crisis”. Journal of Optimization Theory and Applications, vol. 166, no. 3 pp. 1029–1050.

Liu, W. Jin, Z. (2014). “Analysis of optimal debt ratio in a Markov regime switching model”. Working paper, Department of Finance, Latrobe university, Melbourne, Australia.

Nkeki, C. I. (2018). “Optimal investment strategy with dividend paying and proportional transaction costs”. Annals of Financial Economics, vol. 13, no. 1, Article 1850001, <http://doi.org/10.1142.s201049521850001x>

Nkeki, C.I. (2018). “Optimal investment risks management strategies of an economy in a financial crisis”. International Journal of Financial Engineering, vol. 5, no. 1, pp. 1–24, <https://doi.org/10.1142/s2424786318500032>.

Samuelson, P. (1973). “Proof that Properly Discounted Present Values of Assets Vibrate Randomly”. Bell Journal of Economic Management 4 (2), pp 369 – 374. <https://doi.org/10.2307/3003046>

Cox, J. C. Ingersoll, J. E. Jr., and Ross, S. A. (1985). “A theory of the term structure of interest rates,” Econometrica. Journal of the Econometric Society, vol. 53, no. 2, pp. 385–407.

Downloads

Published

Issue

Section

License

Copyright (c) 2026 The Transactions of the Nigerian Association of Mathematical Physics

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.