Binomial Option Valuation Model With Adaptive Swing Factor

DOI:

https://doi.org/10.60787/jnamp.vol69no1.464Keywords:

Adaptive swing factor , Fixed swing factor , Monotonic error propagation, Peizer-Pratt inversion functionAbstract

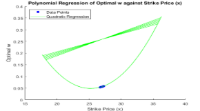

This paper presents a new Binomial option valuation model which is with an adaptive swing factor. The existing versions of the Binomial model are developed based on fixed swing factor and results from fixed swing factor models are commonly associated with Snon-linear error propagations which translates to non-monotonic convergence and reduced accuracy in application to option pricing. In order to overcome this challenge, we adopt swing factors which are functions of the step number(n). The accuracy, convergence and stability behavior of the Binomial option pricing model with adaptive swing factor (up and down move size) are all investigated. The Adaptive Factor Model when compared with two popular versions of the traditional Binomial models - the Cox, Ross and Rubinstein (CRR) model [3], the Jarrow and Rudd (JR) model [5], a more recent Leisen and Reimer (LR) [3] model registered more accurate performances, especially with respect to option pricing.

Downloads

References

Dietmar L. and Matthias R (1996); Binomial Models for Option Valuation-Examining and Improving Convergence; Applied Mathematical Finance, 3, (319-346)

Fischer B and Myron S. (1973); The Pricing of Options and Corporate Liabilities; Journal of Political Economy, 81, 637-659

John C. Cox, Stephen A, Ross, M. R. (1979); Option Pricing: A Simple Approach; Journal of Financial Economics, &, 229-263

Peizer D.B., Pratt J.W. (1968); A Normal Approximation for Binomial, F, Beta, and Other Common Related Tail Probabilities, I; The Journal of the American Statistical Association, Bd. 63, pp.1416-1456

Robert Jarrow and Andrew Rudd (1986); Option Pricing; Irwin, Homewood, IL

Sharpe, William F, (1978), "Capital Asset Pricing Theory: Discussion," The Journal of Finance, American Finance Association, 33(3), 917-920.

Elliott, R. J., Elliott, R. J., Liew, C. C., & Siu, T. K. (2010). “Pricing Asian options and equity-indexed annuities with regime-switching by the trinomial tree method”, Fei Lung Yuen and

Jarrow, R. A. (2008). Financial Derivatives Pricing: Selected Works of Robert Jarrow. Singapore: World Scientific.

Hailiang Yang, April, 2010. North American Actuarial Journal, 14(2), 272-277. https://doi.org/10.1080/10920277.2010.10597589

Downloads

Published

Issue

Section

License

Copyright (c) 2025 The Journals of the Nigerian Association of Mathematical Physics

This work is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.